Base Rates

Base Rates

This week we discuss how to use base rates in investing, index concentration, and shocking opinions of EV owners.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

It’s been a typically slow quarter for us so far. We have added no new positions, and instead looked to add to positions already in the portfolio. But that doesn’t mean we haven't been turning over many rocks to find our next investment. In that search, a recurring concept keeps crossing my mind – that of base rates.

Base rate is an interesting statistical concept that I’ve been trying to incorporate into all my analysis. It’s easy enough to understand, even for those who are less mathematically minded. Let’s say for example that 0.1% of the world’s population are professional athletes and the remaining 99.9% were not professional athletes, then the base rate of professional athletes is 0.1%. Thus, when you meet someone, you are highly unlikely to assume that they are a professional athlete. Further, when someone tells you that they want to become a professional athlete, you know the odds of them becoming one are low, simply because of the base rate.

It’s an important concept to consider when thinking about making an investment. For example, when someone ever pitches a stock and says “This is the next trillion-dollar company” you must remember that in history only about 7 companies have crossed that mark. So, the odds of the unprofitable mid-cap being pitched to you obtaining a trillion-dollar market cap are low. Think of it this way, whenever you’re trying to think through revenue growth rates, or potential market-share, or even valuation – you must think “how often has this happened/not happened before?” And if the odds are against your assumptions, you must have extraordinary evidence for why your assumptions are valid. I think this meme sums up the concept well.

So, with that, let me take you through some of the companies I’ve been looking at, and try to apply the base rate concept to judge their potential success (again, not investing advice!).

Hims & Hers:

Hims & Hers is a telehealth company, which offers drug subscriptions for OTC drugs that treat, well, embarrassing problems such as hair loss and erectile dysfunction. The company has done splendidly recently with (as of March 24) subscribers up 41% yoy to 1.7MM, Revenue on a $1bn run rate, and positive GAAP net income. The stock has responded in kind, up 6.5x since the 2022 lows. It’s become a bit of a cult stock with some bulls arguing that the stock could grow 100x. The company has launched weight-loss drugs, giving the stock an incremental boost over the past few months. All of this makes for an exciting thesis. However, one must pause and think through, at its core what the business is. First, one must remember its selling generics, it is not a pharma company. Second, many of these drugs are OTC, thus many can be bought at your local drugstore or on a few other websites including Mark Cuban’s Cost-Plus Drugs. So, in the end if you boil Hims & Hers to its core parts it is both a DTC (direct-to-consumer) and a telehealth company. So, if you agree with that premise (you may not, but that’s not the point), then you must also think through how many success stories there are. DTC brands like Warby Parker, Dollar Shave Club, Casper, Rent the Runway and Stitch Fix were all the rage a few years back. However, they have lost their sheen. Warby Parker, Rent the Runway, and Stitch Fix’s stocks are down 73%, 95%, and 96% from their peaks respectively. Casper was taken private after a disastrous listing. Similarly on the telehealth side Teladoc and Amwell stocks have lost almost all their value. The story is typically the same. A short-term boost due to a particular event or trend pushes subscribers, revenues, and cash-flows. However eventually trends change, consumers sour, subscribers dwindle and operating leverage works the other way. Again, I’m not saying Hims & Hers will not work out (and I wish stockholders the best), but the base rate is against it working. Thus if it does 100x, it will be the exception not the rule.

CrowdStrike:

CrowdStrike has been a monster of a stock. Up 6x since listing despite a 60% drawdown in 2022. When we were doing only advisory, we had advised a client to buy the stock but then asked the investor to sell when the stock crossed $200 in 2021. We thought for the valuation to hold the company would have to grow revenues by over 40% on average over the next couple years, and you know what, it did. However, the stock currently trades at nearly 100x forward PE. When we did our initial research into the stock, we talked to an employee about the company. He said something that always sticks with me, “leadership always tells us that it's not a matter of if we will get hacked, it’s a matter of when.” And there is plenty of precedent here, many cybersecurity companies have been hacked. SolarWinds, FireEye, Mandiant, Trend Micro, Kaspersky Lab, etc have all suffered. Even Palo Alto Networks recently announced a weakness in their firewall (although I don’t think much damage was done). So, if we listen to the base rates, it's highly likely that CrowdStrike will face a security issue. Now, that won’t be doing the undoing of the company, many firms that have been hacked have survived and bounced back. But at a nosebleed valuation, a chink in the armor can be more like a gaping hole.

NuBank:

NuBank has been another darling stock, and a quick look at the financials one can see why. The company serves almost 60% of the Brazilian adult population. It’s growing its revenues and loan book by 70% and 60% respectively. It’s also hugely profitable with 14% net income margins, and more importantly for a bank, boasts an insane RoE. On a consolidated basis RoE is over 25%, and if you just include Brazil (its next biggest market, Mexico is currently loss-making), RoEs are over 40%. But we need to be consistent with our thinking before we get carried away here. In the end, NuBank is, well, a bank. It will offer many services but at its core it will take deposits and lend money. So, one must look at how Brazilian banks have done over time.

This time, however, the base rates look good for NuBank. Brazilian Banks have a strong track record over the past 20 years, with major banks like Banco do Brazil, Itau, and Bradesco posting on average 12-13% annualized total returns (in USD terms).

Sea:

Long-term readers know I can’t help commenting on Southeast Asia’s tech champ (disclosure: owned). However, 2023 was a rough year for the stock when it was clear TikTok Shop was making inroads into the region. However, this was one of those times when low base rates worked in your favour. While it was only one data point, it was clear to me that even in its most developed market (China), live commerce was only about 20-25% of ecommerce sales. So, my thinking was there was no reason that TikTok Shop should gain more market share than that in Southeast Asia. While market share numbers can be argued, its quite clear Shopee has maintained if not grown its market share and most of TikTok Shop’s gains have come from Tokopedia (which it now owns). This week JPM released a note saying that the economics of social commerce are not viable in Southeast Asia, which if true, will further limit the total market share TikTok Shop can achieve.

Conclusion:

Overall, the base rate concept is an important one to think through, and even the best forgets about it. When asked about his failed investment in Alibaba, the late and great Charlie Munger said, “I didn't stop to realize they're still a goddamn retailer.”

However, there is an irony here, in that, if everyone closely followed base rates we would have a boring world. Very few (and I mean less than 1%) people who join the corporate world become CEOs, but it’s a good goal for many. If every budding actor looked at the success rates in the industry and chose a more stable profession, we wouldn’t have a Tom Hanks or a Sridevi. ~50% of marriages in the West end in divorce, but that’s a bad reason not to get married. Starting a company has an overwhelming chance of failure, but the world’s economy would be nowhere without entrepreneurs. Most funds (and stocks for that matter) don’t outperform, but we try anyway.

The point of using base rates as a framework is not that if the base rates are against you that you shouldn’t invest. Just ask early investors in Amazon, Tesla, and Southwest, all of whom bucked the trend of sleepy industries. But what base rates do is help put sanity around your assumptions and make sure you’re not getting carried away with the thesis. For example, for all the Nvidia bulls, how many stocks that have gone up 10x in less than two years go on to double again in short-order? How many have instead corrected 50%? Worth thinking about.

Thanks for reading, and happy investing

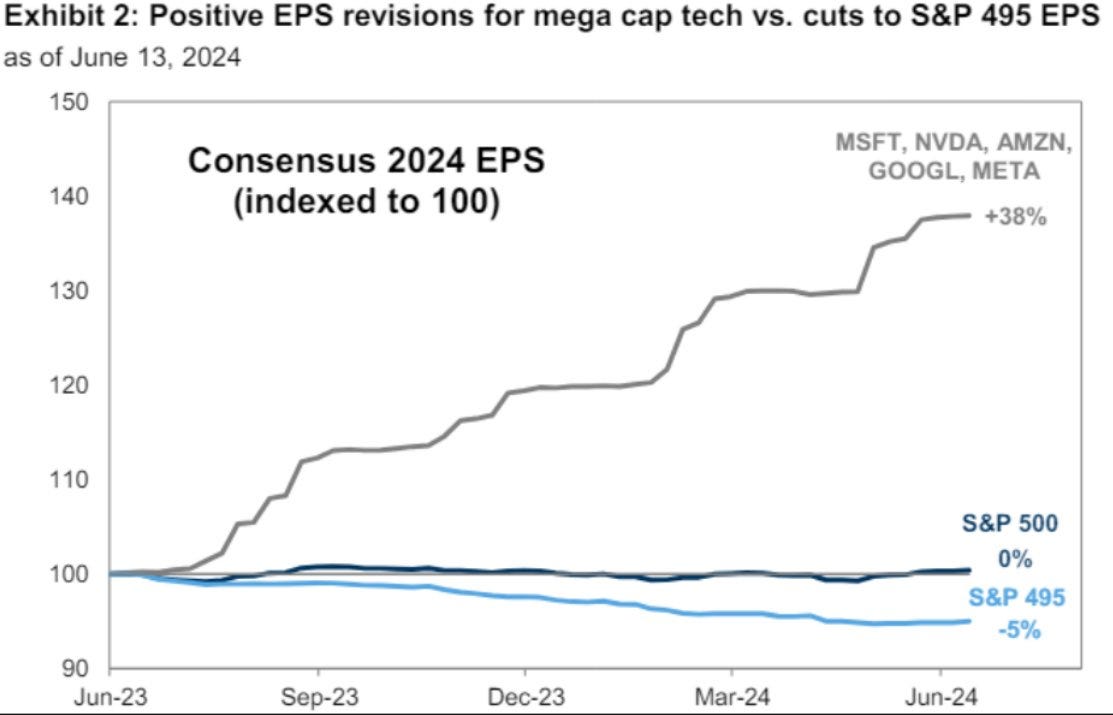

Chart of the Week

Concentration of Profit - This is quite a chart, showing that most of the profitability growth of the S&P is driven by just five stocks. (source)

Links of the Week

This might be the most surprising article I’ve read recently. Turns out almost half of EV owners want to go back to gas cars.

What’s really happening in software? This post lets you know. It goes into interesting details about budget reallocations.

There’s significant debate about if the US markets are too concentrated, this paper explores if that’s the case.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’ or share it. Thank you!