Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

“Do Nothing. When you have no move Mr. Thompson, you do nothing… I’ve made my living in large part, Mr. Thompson, as a gambler. Some days I make 20 bets. Some days I make none. There are weeks, sometimes months, in fact, when I don’t make a bet at all simply because there is no play. So, I wait, plan, marshal my resources, and when I finally see an opportunity, and there is a bet to make, I bet it all” – Arnold Rothstein, Boardwalk Empire.

Boardwalk Empire was a highly entertaining show, but mostly taught the wrong lessons about life. That said, it often had some deep wisdom embedded within the gun fights. This one, uttered by a character based on the real Arnold Rothstein (an American racketeer and crime boss who fixed the 1919 Baseball World Series) always stuck with me.

In investing, especially long-term investing, we tend to want to act. It’s difficult not to. We, as humans, have a biological need to do something. If you didn’t run when the grass was moving, it likely meant you got eaten by the lion. If you didn’t take cover when the volcano exploded, it probably means you got covered in ash. Action is inbuilt in us. But usually, when it comes to investing, there isn’t that much to do. Ideally, we have a good 3-4 ideas a year (in a productive year), and the rest of the time is spent saying ‘no’ to new ideas.

It’s hard to explain this to people who don’t do what we do. My wife will often ask me how work was and I reply with the standard, “It was fine”, and then she naturally follows up with “what did you do?” and most often my answer is, “nothing much.” Most days are spent reading, modeling, sleuthing, digesting, and speaking to those in the know (other investors, experts, etc.), but very rarely does any of this result in action. So, when I say “nothing much,” it’s not that I surfed the internet all day laughing at memes, but that many times, days and weeks will go by without anything tangible to show for it.

You may have already heard this podcast (I highly recommend it if you have not listened), but Nicolai Tangen was on the “Value Investing with Legends” series. Tangen is the CEO of Norges Bank Investment Management. The Norges Bank, Norway’s central bank, controls the largest sovereign wealth fund in the world, which Tangen oversees. He hit the nail on the head in the podcast when he said – “You come home from work, your husband or wife asks you, “What have you been doing today?” “Well I’ve done nothing”. Next day, Tuesday “what have you been doing today”, “nothing”, Wednesday “nothing”, Thursday, “nothing”, Friday, “nothing”. You just feel like a failure. So therefore, you feel like you have to trade a bit. But it is mostly not very profitable.”

Inertia is hard to be comfortable with, and that makes sense. In most jobs, inertia will get you fired, or run over by competition. But in investing and portfolio management, it’s almost a requisite. Another exercise that Tangen recommends is to compare your portfolio at the end of the year versus your portfolio at the beginning of the year. “Take your Jan 1 portfolio, run it for the full year without any changes, and see how it ends up. Then you look at your actual results. and that tells you this. It is just awful sometimes. That there are years when you go to the office every day and the only thing you manage to do is subtract value.”

I internally run this exercise every year, and some years the results are humbling. That said, it's just a data point. For example, having a portfolio going into 2022 which was short tech and long oil would have been incredible, but that would have been not so great to hold during 2023. So annual results tell you only so much. Regardless, the Jan 1 portfolio comparison is a useful process to derive insights into your decision making.

The question is then how we improve decision making. The answer circles me back to the quote above from Rothstein, do nothing, or at least do less. This is almost counterintuitive though. How do you get better at basketball? Shoot many baskets. How do you get better at cooking? Make many dishes. In almost all skill sets, doing more, not less, is the path to victory. However, we already have significant decision-making practice. The average human makes about 35,000 “remotely conscious” decisions a day. Many of those are small decisions, like picking up your coffee cup. But we also make around ~122 informed choices a day (i.e. from deciding on lunch or on what to say to your partner when asked what you did that day). So, we are getting our batting practice in.

Further, the act of “saying no” or “doing nothing” is a decision. For example, I get a lot of excitement out of reading an annual report of a company I just discovered. For investors, it’s kind of like opening a new present, there’s an excitement that you might find gold underneath the wrappers. However, just like most presents, a few pages into the report, the excitement changes to disappointment (or confusion when the investment is out of your circle of competence). Most often than not, the annual report is as far as you will get into a potential investment, as you make the decision not to pursue the investment any further. There end up being only a few investment discoveries in the year that really get your blood pumping and mouth salivating, and that’s where, to Rothstein’s instruction – you bet it all (ok I don’t mean this literally, don’t be crazy).

As this year ends and the new one rises, I often take some time to reflect on what I want to improve about myself over the next year (personal and professional). Within the “professional” bucket one of my goals in 2024 is to do less. To say ‘no’ more, and resist the urge to act. I still must think through how I measure this (maybe the number of times I trade in a year?) but doing less seems to be a preferable method of operating.

On another note:

It’s been a fascinating 2023, and with major indices reaching or passing through all time-highs, it seems like the market has put the drawdowns of 2022 firmly behind it. There is a definite sense of triumph for the bulls now that the Fed has “declared victory” over inflation and is looking to cut rates in 2024. However, I do think that rate cutting isn’t necessarily the fuel to rocket the markets up. Brazil, which had nearly 14% rates going into 2023 started to cut this year and is now at 11.75%. The initial move for the market post the first cut was down 7% in the subsequent months (although it has since recovered). So, it could continue to be a rocky 2024 even though the overall environment seems to be de-risked. But, since it is the end of the year, let’s make some predictions for 2024. I will urge readers to put very little weight behind these, it’s just for fun.

Small and mid-caps outperform large caps: Most of the gains in indices this year have been driven by the “Magnificent 7”. As interest rates are cut, mid and small caps which are perceived to be ‘riskier’ get bid as discount rates reduce. Further I also saw an article that Russell 2000 companies have nearly half their debt in floating rates, where less than 10% of S&P 500 debt is such. Thus, rate cuts should disproportionately benefit smaller companies.

Asset managers do very well: This cringe Blackstone video aside, capital raising unlocks as allocators chase the market. Lower discount rates mean higher valuations, increasing marked values, as well as realizations.

Crypto comes back in vogue: I have a tough time understanding how crypto is anything but a speculative asset, but lower interest rates will increase the propensity to gamble.

Major indices do worse (or less well) than this year. We are going into 2023 with the top 10 stocks accounting for 31% of the weight. Many of these companies are going to see at best high-single digit growth given large base rates. Let’s take Apple for example. Street estimates assume about a 5% average top line growth and stable margins going forward. EPS will increase in the high-single digits due to buybacks, but the stock is already trading at a 31x forward P/E ratio. It’s been here before, in 2008-09, but EPS grew at an astonishing 100% CAGR over the next 3 years. So, it’s a tough valuation mountain to climb. But, I’ve been saying this for years.

We’ll touch base in 12 months to see how accurate any of these predictions were.

Lastly, I wanted to give thanks to all of you, our wonderful readers. It brings me great joy and satisfaction to see how many of you have read, enjoyed, liked, and shared this newsletter over the years. We have readers from 67 different countries, and it boggles my mind at times that such a far-reaching audience has an interest in what I have to say. So, from the bottom of my heart, thank you.

We’ll chat again in 2024, until then I wish only one thing for you all. Relax, spend time with family and – do nothing!

Thanks for reading, and happy investing.

Happy Holidays,

Pratyush

Farrer Fun Fact

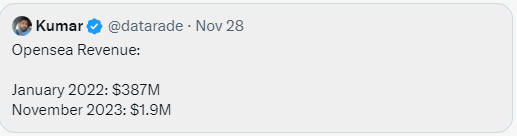

Hype-train Derailed: OpenSea was one of the leading NFT marketplaces. The data above shows how quickly the broad market lost interest during the 2022-23 crypto winter. Though I do suspect some bounce-back in 2024. (source)

Links of the Week

This was fun video of Charlie Munger’s greatest zingers. RIP.

I really enjoyed this post about the “infinite ladder” of success and happiness.

Last one on Charlie, in one of his final interviews, he has a 90+ minute conversation with Stripe’s John Collison. Its filled with wisdom about investing, China, and the future. Give it a listen.

For those who follow Evolution - this was a fantastic podcast covering the bull and bear cases relating to the company. Well done Ali and Graham.

More for the diehards - but I read this new Michael Mauboussin paper on Pattern Recognition over the weekend. It explains how investors over rely on pattern recognition when in reality it only works in certain circumstances.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’. Thank you!