Durable

Durable

This week we discuss durable business models, PE dispersion, and "active patience"

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

Happy new year to all! Hope you managed to spend some time with your loved ones and had a chance to recharge.

Over the break I listened to this Business Breakdowns episode about Moody’s. As most of you would be familiar, Moody’s is the largest credit rating agency in the world. It’s had a solid financial performance over the last twenty years with Revenue and EPS compounding at 9 and 11% respectively, and thus is described as a high-quality, high-moat, steady business.

While it certainly is all those things, the podcast brought up a fascinating point that I’ve been thinking about recently. In the aftermath of the GFC in 2008, rating agencies, such as Moody’s were the target of much public and professional vitriol. Afterall, it is the rating agencies that gave sub-prime mortgage linked securities the AAA ratings which allowed for financial institutions to hold them on their balance sheets’. It was in the aftermath of this furor that US regulators opened the list of nationally recognized statistical rating organizations from three to 10. However, as the podcast brings up, this regulatory change should have killed Moody’s moat, but it didn’t. Even despite their colossal screwup leading up to 2008, the company went from strength to strength. In fact, since the lows of 2009, Moody’s stock is up 21x! Even after facing the wrath and influence of both US regulators and its political class it survived, and as the stock and financial performance shows, thrived (thank you to my friend Jeremy Deal for the verbiage).

This analysis got me thinking about other businesses that survived near-death experiences but later thrived, and if this character building experience could be an interesting hunting ground for future investments. The thinking is, if this event didn’t kill them, nothing else will. However, before we can start our search, we must be clear about what we are looking for. Thus, we must define what a near-death-experience is.

I can’t say I have a complete definition of what a near-death experience for a company looks like, but I think one (or more) of the following must be true.

Regulatory change that makes investors question the long-term viability of the business.

Product/branding failure which makes customers lose trust in the brand.

Technological change that impairs business and forces the company to change their core offering.

A geopolitical or global event which temporarily but deeply impairs the operations of a business.

Internal scandals/accounting failures that lead to a significant loss of trust from the consumer or investor community.

The final part of the definition must be that they survived, hence the “near-death” part of the term. For example, the likes of Polaroid, Enron, and Blockbuster would not qualify. Given these examples, identification of a ‘survivor’ of a near-death experience may not be clear for several quarters or even years after the event has occurred. So, its quite likely that even if you suspect one, it could be a while before you get the ‘all clear’ signal (if you get it at all).

But, I’m getting ahead of myself. It would be important to first test the criteria above, and see if we can find past and potential examples.

Regulatory change that makes investors question the long-term viability of the business.

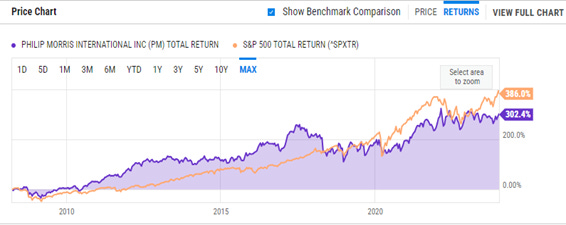

Philip Morris:

The easiest example here is tobacco companies, which, for years, have been targeted by Western governments for obvious reasons. However, several companies within the vertical have done a decent job of staving off disaster. Philip Morris, for example, has kept pace with the S&P 500’s total return over a 15 and 5-year period (the S&P only started to pull ahead in the back half of 2023). Further on each 1-, 3-, 5-, and 10-year period the stock has delivered a positive total return (buoyed by its hefty dividend).

It seems to have done this by quickly pivoting from combustible tobacco products (ie traditional cigarettes) to smoke-free categories, the latter of which now make up 35% of net revenues. Further over the past 15 years both Philip Morris’ revenues and EPS have shown growth. This is after major regulations like the Family Smoking Prevention and Tobacco Control Act in the US, the Public Health Act of 2007 in the UK, and global packaging laws and menthol cigarette bans. So, while no future can be certain, it's clear that a slew of regulation has failed to kill Philip Morris’ business.

Coinbase:

Similarly, I have found the case for Coinbase interesting. Here is a company that survived a crypto winter, a Wells notice from the SEC, and increased competition in the form of Bitcoin ETFs. Yet, the stock was up 4x last year (granted after a 90% drop in 2022). But it seems to me that the company is in a decent position. Its outlasted large competitors like FTX and Binance and it does not seem to be run by bad actors (I could be wrong here though). Further, it's quite likely that trading volumes have bottomed for the time being. If Coinbase can get through this upcoming hearing regarding the SEC’s case against them, this might be one company that can’t be killed.

Product/branding failure which makes customers loose trust in the brand

Dominos:

Most market participants would agree that Dominos has been a monumental success, and that long-term shareholders have been handsomely rewarded. Further most consumers would know Dominos for its decent pizza that’s layered with speedy delivery and a convenient app. However, in 2010 the company went through a crises of consumer revolt. For a period, consumers ranked the taste of Domino’s pizza amongst the worst of its category. So poor was its branding that in blind-tests consumers would rate Domino's pizza’s even lower after finding out which brand they came from. But Dominos was not to be undone, and embraced the customer feedback hard. They turned the crisis into a marketing campaign and a chance to rebrand themselves and redo their recipe (it was so clever – watch this video). The turnaround worked and since the stock is up 51x since!

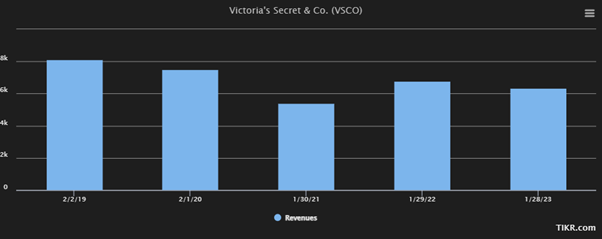

Victoria’s Secret:

Victoria’s Secret was the lingerie brand for several years, and as recently as 2013 it had a 1/3 of the market share in its category. However, over the past decade a series of marketing missteps/trend falling has led to plunging sales. It targeted a more ‘inclusive’ messaging which was a deviation of its previously ‘sexy’ and ‘exclusive’ brand. This pivot turned out be quite a disaster with plunging sales (From 2019 to 2021 sales fell 33%)

It was announced a few months ago that the company would go back to the branding that made it famous (think Victoria Secret Angels) and bring ‘sexiness’ back to the brand. While YTD 2023 sales have still been poor (down 10%), this could mark a bottom for the brand. If the turnaround is successful, the stock could be a bargain at a 10x PE ratio.

Technological change that impairs business and forces the company to change their core offering.

Netflix:

People often look at the most recent result and forget history. It’s quite clear now that Netflix has come out on top in its streaming wars. However, they almost had a meltdown in 2011 when it lost 800K customers overnight (this was when they had 10% of the users they have now). The crash was self-inflicted in the sense that the company changed its subscription model from around $10 for both renting and streaming to $8 for each individually. Netflix was forced to this for two reasons (I believe). One, they saw the popularity of YouTube and the streaming model take hold, and couldn’t stand to lose that ground, and secondly, Blockbuster had started ramping up its mail-based rental model (which is how Netflix started). As Hastings (CEO) put it:

“For the past five years, my greatest fear at Netflix has been that we wouldn't make the leap from success in DVDs to success in streaming. Most companies that are great at something – like AOL dialup or Borders bookstores – do not become great at new things people want (streaming for us) because they are afraid to hurt their initial business. Eventually these companies realize their error of not focusing enough on the new thing, and then the company fights desperately and hopelessly to recover. Companies rarely die from moving too fast, and they frequently die from moving too slowly.”

Consumers revolted however and saw this as a cash grab. It took several quarters for Netflix to win customers back, with a superior product, more content, and the fact that streaming was obviously better than rental. Since the 2011 lows, Netflix is up nearly 50x.

BPO Industry:

The BPO industry is now facing its ‘come to Jesus’ moment. Services like customer support and content moderation are all under threat from AI. Further, I’ve noticed over this past cycle that customers who traditionally would cut costs by outsourcing, are instead automating processes internally using AI-based tools. I’ve spoken to several experts who put the level of revenue cannibalization at between 20-40% due to AI. Stock prices of major BPO players have fallen 60-80% from their peaks. That said, the BPO industry has been here before, when chat bots came around, commentators believed that this would mark the end of the industry. However enterprising companies just folded chat bots into their offering and made their overall businesses more efficient. The same could happen with the AI threat, so I do think the industry warrants a close eye.

A geopolitical or global event which temporarily but deeply impairs the operations of a business.

Major Banks:

2008 was an insane time for banks. Lehman failed, Bear Sterns was bought out, Bank of America and Merrill Lynch merged. Washington Mutual collapsed along with several regional banks. All this was also just in the US. While for the banks that ‘made it’ their businesses weren’t impaired per se they certainly had to change the way they used their balance sheets. Some banks (i.e. Citi) recovered but never really thrived, however banks like JPM, Wells Fargo, and BAML have done quite well. JPM’s stock has handily beat the S&P 500 over the past 10 years. Wells Fargo hit an all-time high in 2018 (but then has had other issues), and Bank of America did have a near 8x recovery from its GFC lows. Now, it's clear that these institutions can’t operate the same way they did pre-crisis, but it's also clear that they are now all “too big to fail '' making their businesses quite durable.

OTAs:

Similarly, the covid-crises brought Airline and OTA businesses to a screeching halt. Airlines, in my opinion, remain a tough business due to their asset-heavy nature, but I am quite surprised we have had no major airline financial failures since the covid-crises. While we did have some mergers, and some smaller players did collapse, overall, none of the major international carriers filed for bankruptcy.

Secondly, many OTAs have done well to make themselves more cost-efficient post-crises. Bookings and Expedia both generate more revenue and operating income now then they did in 2019. We have held a position in eDreams (Europe’s largest OTA by flights) for several years, and this has been their financial performance since covid.

Covid ground travel to a halt, and yet several players in the space not only survived but thrived as well. We reckon the future is bright for companies that have such durability.

Internal scandals/accounting failures that lead to a significant loss of trust from the consumer or investor class.

Starbucks:

One of my favourite parts of Shrek 2 was when the crowd was running away from a giant gingerbread man, and they ran out of one Starbucks and directly to another one right across the street. It was hilarious but also a testament to how successful the chain had become. However, investors (myself included) forget that Starbucks had a rough ride in 2007. For one, a shift in consumer behaviour away from large chains to local businesses and ethical practices. Howard Shultz (founder) started to delegate tasks away which led to a drop in client satisfaction as standards fell (i.e. shipping coffee grounds instead of whole beans). Things got so bad Shultz penned a memo to the then CEO titled “The Commoditization of the Starbucks Experience” which was leaked to the press. There is a great article about this that can be read here. The company’s stock fell 40% that year. Eventually, Shultz got back in the driver seat and righted the ship. Since the end of 2007 though, the stock has rallied nearly 10x.

Luckin Coffee:

While, in my opinion, a worse situation, Luckin Coffee was once a darling of Chinese stocks. Its rapid expansion impressed the market, and their post-IPO valuation hit almost $15 billion. However, an accounting scandal in 2020 rocked the company when it was revealed that they had been over-reporting revenues. The company was investigated by both US and Chinese authorities and the chairman of the company defaulted on a half a billion-dollar margin loan. The company had to file for bankruptcy in 2021 and was restructured. If I’m not wrong, almost all top management was replaced. But since then, the company has staged quite a comeback. It continues to expand both in China and internationally. In fact, I can’t turn my head without seeing another Luckin Coffee store in Singapore (the Shrek joke comes full circle). Post bankruptcy the stock fell 98%, but has since rallied 8x, and is now trading around the same levels it was at post-IPO.

Now granted, maybe this isn’t a ‘near-death’ experience – if you file for bankruptcy, in my opinion, you died. But the company was resurrected, and since then has gone from strength to strength. With a new PE owner at the helm, and a product that seems to really resonate with customers, it does seem the business is more durable than ever.

To wrap up, if we can thread a needle through all the examples we used above where businesses did well after their near-death experience, I do think it comes back to the deep moats of the business. Moody’s survived because they had a product moat – their ratings were ubiquitous globally. Tobacco continues to do well due to a combination of regulatory moat (no one really wants to enter the traditional cigarette business) and a brand moat that allows them to raise prices. Netflix has significant scale advantages. Starbucks and Dominos probably relied on their low-cost production to maintain cash flow as they revived their businesses. Thus, to assess a potential thriver, the moat of the business needs to be studied deeply along with the near-death event itself.

If you have other examples of potential businesses that are in the process (or have just) suffered near-death experiences, feel free to list them in the comments.

Thanks for reading, and happy investing.

Farrer Fun Fact

Dispersion: One of the key issues with investing in PE/buyout funds is the huge dispersion in returns between funds. Thus if you pick wrong, you’re likely to endure significant opportunity cost. The chart above shows quite clearly how wide the range of performance is for PE vs public market funds. That said, the overall returns can’t really be compared like this as PE funds use IRR where as public market funds use CAGR. (Source: KKR)

Links of the Week

Put these charts on your wall. A fascinating video that shows the main lessons learned in 2023 using charts.

A thoughtful letter to anyone who wants to start their own fund.

Ian Cassel explains what ‘active patience’ is and how long it takes to know yourself as an investor in this writeup.

An insightful interview featuring Stephen Mandel, one of the investing greats, about how he spends much of his time thinking about people.

A lack of Chinese tourists is hurting Orchard Road sales in Singapore, as explained by this article.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’. Thank you!