Interruption

Interruption

This week we discuss interruptions, Sea's earnings, and how stock market charts can be highly misleading.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Latest Blog Post

Dear readers,

I apologise for not publishing posts in a more regular fashion. However, I’ve taken a decision to write only when I think I have something interesting to say/comment on, and often, weeks go by before this occurs. This hopefully increases the quality of the content and lowers the clutter in your inbox. Further – I may cover two or three topics in one post (sometimes related, and at times, like today, unrelated). This is in case there are several topics worth covering in the weeks since the last post and for readers to focus on what interests them. Thanks for reading and happy investing!

Okay, on to the post.

Interruptions:

For those who follow the Indian market, Rakesh Jhunjhunwala was a titan. Known as “India’s Warren Buffet,” he was one on of the best-known investors in the Indian stock market. Probably more of a mix of Buffett and Druckenmiller than a direct comparison to the Oracle of Omaha, the Oracle of Dalal Street was undoubtedly a skilled money maker. At his passing last week, at age 62, he was thought to be worth ~Rs. 32,000cr (US$4bn) when he allegedly started with just Rs. 5,000.

While Jhunjhunwala had more money than anyone really needs, the compounding of his wealth has essentially ended with his early demise. It was interrupted. Without trying to sound callous, I couldn’t help but wonder how much he would have been worth had he lived to the age that Warren Buffet is now (nearly 92), or another 30 years.

If he had compounded at 14% (the Nifty’s annualized capital gains over the past 20 years), he would be worth over $200bn and 98% of his wealth would be created during this time.

If he had compounded at just 7% (India’s annual GDP growth estimates over the next few years), he would be worth over $30bn and 87% of his wealth would be created during this time.

Heck, even if he completely lost his touch and compounded at just 4%, he would be worth $13bn and 70% of his wealth would be created during this time.

The point here is not the annualized return, but the time spent compounding that matters. In the equation where Returns = Capital * (1 + Rate of Return) ^ Time, it’s the “Time” variable that has the largest impact on the final figure.

Thus, interrupting the compounding process is the one action that has the largest impact on your returns (obviously assuming returns are positive). Interruptions come in many ways and tend to be felt acutely during bad times.

For the individual investor:

Poor health causes interruption: Either to fund unforeseen medical expenses, or in the worst case, death.

Leverage causes interruption: Drawdowns will force you to sell when you don’t want to.

Spending above your means causes interruption: The more money you need, the more you take out of your investment account.

Divorce causes interruption: At least half your money stops compounding.

For the fund manager:

The wrong LPs causes interruption: LPs who don’t understand the strategy or have different goals may cause redemptions at the wrong time (this is the fund manager’s fault for not setting expectations well).

Leverage causes interruption: Just ask Bill Hwang.

Heavy shorting and use of options cause interruption: They have a high likelihood of leading to permanent capital loss.

As Charlie Munger said, “The first rule of compounding: Never interrupt it unnecessarily.” Now, death cannot be avoided, but almost everything else discussed above can be. However, even death can be delayed – so staying healthy is vital.

Sea Update:

Speaking of (or the opposite of) healthy, Sea Limited reported its earnings this week and was met with the market’s disappointment. We have been public about the fact we do hold Sea’s stock in our managed solution but have been trimming the position for a while. While it’s not normal for us to comment on our portfolio holding’s earnings, we do know Sea is a heavily followed business in the region not only because of how well its stock did in 2020 but also because of how ubiquitous Shopee has become. Thus, we thought we’d share our views. As always, none of this should be considered investment advice – and we may choose to add to/reduce/remove our position at any time.

Sea’s story has changed from one of incredible growth to one of profitability in a matter of just three quarters. While the expectation was that 2022 was going to be a tough year for comps in gaming business (especially after Free Fire was banned in India), investors were placated (or perhaps fooled?) by guidance at the start of the year that the e-commerce business, Shopee, was going to grow revenues by 75%+. That dream became a nightmare after management pulled its guidance this quarter. In hindsight, given that even coming into this year GMV growth had come off to 53% yoy and was likely to simmer down further as the year progressed, it was silly for us to think the gap could be made up by rapidly increasing Shopee’s take rate. So, shame on us for that.

Earnings were not ALL bad though. There were some positives, such as Garena showing stability in its Quarterly Active Users (paying users still needs to stabilize), Digital Financial Services growing at breakneck pace and filling in some of the Garena-shaped gap in the top-line. Even though Shopee guidance was pulled, it did grow Gross Orders by 42% yoy whereas Lazada (largest regional competitor) only grew their orders 10%, implying that Shopee is expanding its already sizeable lead.

The difficulty we now see on Sea is twofold. One is of cashflows and the other, of valuation.

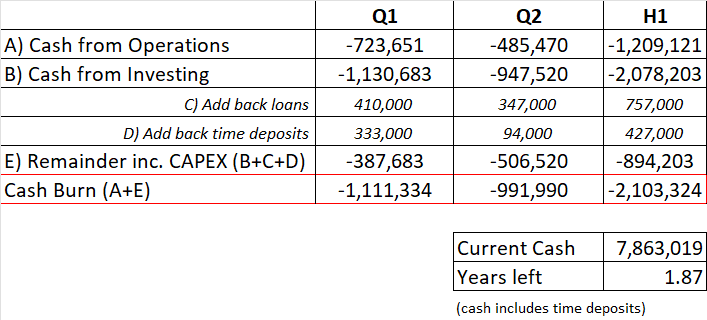

Cashflows: As you can see from the below chart, the company has little time left if it maintains the current level of cash burn. There is also a long-term issue of the 2025 and 2026 convertible bonds (combined notional value of nearly $4bn) which are out the money (the 2026 one is deeply so). So, what investors should hope for in subsequent quarters is that burn coming down drastically. It does appear that the burn peaked in Q1 so declines, I believe, are guaranteed. It’s the pace of declines that is unclear and only time will tell. That said, management has stated that their key businesses would be at least break-even by next year (except for Shopee Brazil) so it’s quite possible that this cash burn looks worse than it really is. The other risk is how much growth will need to be sacrificed to bring this burn to neutral levels, and it appears that even management isn’t sure of this, as if they had been they would have just revised e-commerce guidance instead of pulling it all together.

Valuations: The criticism I’ve heard from investors is that Sea, in their bid to make Shopee’s SEA business break-even after corporate expenses, is shifting expenses around. It doesn’t help that Sea has notoriously poor disclosures so trying to strip out various costs becomes difficult. However, I’m of the opinion that this really doesn’t matter. In the end, shifting costs around could make one business seem profitable at the expense of another, but the cashflows of the overall business are what investors need to focus on (bringing us back to the above point). If you do reach this conclusion, however, you face another problem which is how to value Sea. As our friend Punch Card Investor pointed out, Sea was typically valued as the sum of the parts of its various businesses, and generally the market was giving Shopee (high growth) a higher multiple and Garena (low to no growth) a lower one. But by focusing on aggregate cashflows you end up having to value the business on a blended basis, which is tough to do. That said, the street seems to think that Sea’s free cash flows will reach around $2.2bn by 2025. If you apply a low-single digit free cashflow yield you do end up calculating a valuation much higher than the current one. The validity of that free cashflow number is where the problem lies, and investors will need to take the over/under on it.

Sea has not been an easy hold these past nine months, and the next two quarters are going to be quite make-or-break for the company with regards to investors’ faith in management. If management does succeed in rapidly bringing down the burn without totally scuttling growth, then the upside on the stock price looks quite attractive at these levels – but investors will have to decide for themselves if that upside is worth the risk.

Thanks for reading, and happy investing.

Farrer Fun Fact

A fake rally? We recently saw crypto prices try to set a steady march upwards, however it seems that this trend was driven by low near-term volumes, implying that this rally did not have legs. The decline over the last few days is proving this assumption correct. (source)

Articles and Videos of the Week

This image is all the “macro” data you need to consume for now. Investors have been circulating a chart showing how recent market moves are almost identical to those in 2008 (implying significant downside). Turns out you can find any chart to fit your mood/mindset.

This tweet illustrating Google’s 2000 financials as mind boggling. Revenue has grown ~13,500x since then.

We really enjoyed this article on Mexico’s development issues. Like the author we’ve always struggled to understand why Mexico has not reached its potential given its dynamic population, decent infrastructure, and size. This article tries to solve that puzzle.

Start of a tech winter? A really well researched post on the rapid changes in mega-tech hiring and how that effects job seekers and hiring managers.

Visa & MindGeek. This article is not an easy read, but an important one. It illustrates how the world’s largest payment networks such as Visa could be complicit in the most vile online activity.