Mashup

Mashup

This week we discuss everything on my mind, Omaha, and Ken Langone's wisdom.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

Mashup

I was writing a blog post but it just didn’t come together like I wanted, so decided not to hit send. But I did have a number of ideas I was mulling through so thought it was worth presenting the mashup below.

Meta

I’m a bit surprised that the market was surprised by Meta’s stock’s post-earnings reaction (-10%). The comments I read were annoyed at the market for punishing Zuck for investing in the future of Meta. But investors forget, Meta is a jockey bet and it can be disconcerting that a founder who has ultimate voting power is stepping up expenses. Its even harder when the ROI (esp. on Reality Labs) is just not clear. Investors still have PTSD from 2022.

Retail

A couple month’s ago I read a post from Andrew Walker, who writes the popular “Yet Another Value Blog.” In it, he said “I talk to a lot of investors. One of the things that I think separates the best investors I talk to from the “also rans” is how inferior investors become attracted to “spreadsheet math.” Inferior investors spend a lot of time in excel, and when you spend a lot of time in excel you tend to invest in things that work really well in excel, and your answer to most questions you get asked about a business will tend to focus on the spreadsheet math, not a fundamental understanding of the business.”

I’ve been thinking about this concept recently, especially as it pertains to investing in retail. Retail modelling can be a real trap, as its easy to do. You know one unit produces X amount of revenue at Y profit so you can clearly model out future cashflows - #of Units * X * Y. However, this is usually where the wheels come off, as the interest rate environment (retail tends to come with debt), competition, consumer behavior, maturation all matter. We have two retail investments, one doing quite well and the other less so - the funny bit here is that our models were quite accurate, but numbers only tell part of the story.

Stories vs Numbers

On that note I’ve been fascinated with the stories versus numbers concept lately. In particular, two stocks have been on my mind to think the concept through. The first is Matterport. The company was a SPAC darling that was built on a story (something about the future of 3D Spatial Modeling). Its stock fell 93% from its peak and stayed there until this week’s buyout announcement. The decline was driven by hype without substance. Just take a look at magnitude of their overpromise in their filing presentation (2021).

On the other hand I’ve been thinking about Nike. The numbers don’t look great. Its stock has fallen ~50% from its peak. Single digit growth, declining returns on capital, and shrinking market share are expected going forward. But this is the company that invented the modern running shoe. This is the company that despite its scandals (labor/environment issues, Tiger Woods) has compounded its stock at a near 20% CAGR for the past 40 years (not including dividends). To invest in the stock now you must believe the story that they will innovate, regain market share, and thrive once again.

I think if you were to break down any solid long-term investment it requires three ingredients. A good story, strong numbers, and a catalyst.

Obviously there is more complexity here as you can see from the below table. But sometimes growth investors get caught up in the story and forget the numbers and value investors get caught up in the numbers and forget the story. Both are risky approaches to take.

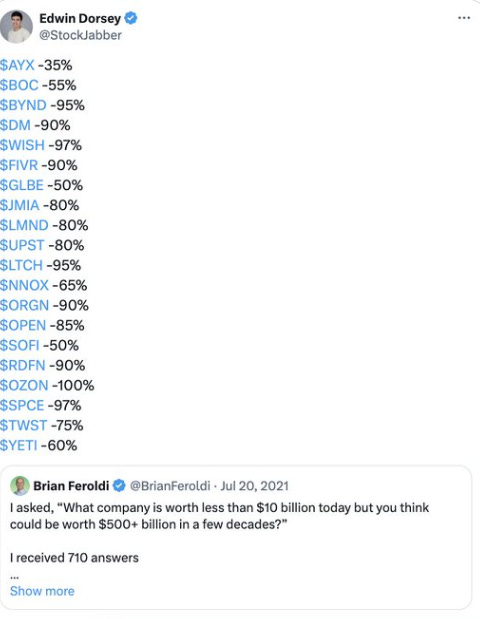

The wisdom of crowds

This was quite jaw-dropping. in 2021 a Twitter analyst asked his followers for the greatest growth opportunities. This week, another analyst posted the results of the top ‘20’ opportunities and it was quite a sight.

Beware of the wisdom of crowds - its likely masking madness. The problem with almost all of these companies is that their theses was built purely on stories - without the numbers to back up them up.

China/Hong Kong

On the topic of the wisdom of crowds, over the past ~3 months the Heng Seng Index has rallied nearly 18%. KWEB (an ETF tracking China tech) is up 25%. It might be just a short-term rally, but given we are at peak negativity relating to China, this could be an interesting pond to fish in (not investing advice). Especially given that pockets of US tech are showing struggling signs (Tesla/Apple), I imagine investors will start to look elsewhere for tech exposure. (ahem… Sea).

TikTok Ban

Speaking of China, I think this is the beginning of the end for the social media giant (ex-mainland). China will not allow a sale, and the company has already started calling the bill a “ban”, which it is not. Me thinks they are conceding defeat. Some argue the rest of the world is still their oyster, but I reckon once they loose the US then the network effect unwinds quickly. Like it or not, the US is still the greatest exporter of culture, and once you loose top American influencers to other platforms, globally, the entire platform weakens. Time will tell.

Omaha

Lastly, I’ll be in Omaha next week for Berkshire’s AGM. I’m curious how the event will feel now that Charlie is no longer around. I imagine it will be a bit like the time I saw Guns N’ Roses play without Slash. Still great, just not the same. That said, the weekend is probably the best event in our industry for networking, so if any of our readers are also attending, please do say hello!

Thanks for reading and happy investing.

Chart of the Week

Filter: This was a fascinating chart of how IMC filters investments (source). That said, as MSCI showed this week, there is a cost to overpaying for quality.

Links of the Week

This episode of “Invest like the Best” was well, simply one of their best. Ken Langone is a living legend and as one of the founders of Home Depot he has significant wisdom to share. Its a short episode, so its very worth your time. Do note the audio isn’t the clearest.

This is an interesting table of how US Teens rank brands over the past few years. Despite the loss of market share Nike remains a hugely popular brand (believe the story!)

Why Grab failed at becoming a super-app is well explained in this writeup.

There is risk in not taking risk, as Howard Marks explains.

For those going to Omaha this is a great list of all the events occurring during the weekend.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’ or share it. Thank you!

Loved it

Thoughts on story vs numbers