Panic, Capitulation, or Anger? (Part 2)

Panic, Capitulation, or Anger? (Part 2)

This week we review where we are in the market cycle, highlight the ponzi that is GoTo, and remind ourselves that investing is hard.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Latest Blog Post

Panic, Capitulation, or Anger (Part 2)?

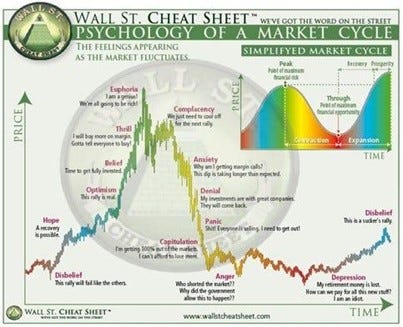

I published a blog post on May 22 this year displaying the above chart to try and understand where we were in the market cycle. In that writeup, I stated that I felt that the indices were somewhere between panic and capitulation whereas several individual stocks were firmly in the capitulation stage (esp. non-profitable tech). I think I was quite right about the latter. The poster child for non-profitable tech is Cathy Wood’s ARKK fund, which when compared to the chart above, is almost an exact replica.

If this isn’t in a clear sign of the “Anger” stage – I’m not sure what is.

However, I do think when I wrote the original post, I was a bit too optimistic about the indices. I think rather than panic and capitulation, they were probably closer to the denial stage. To be fair to myself, I did say that most of the market stalwarts (Apple, MSFT, etc) were still in the ‘denial’ stage, but likely misjudged the indices a whole. Since then, the S&P 500 has fallen about 9%, the MSCI All-World Index is down around 11%, and the Nasdaq is down around 9% (as of Friday morning Asia time). The relative outperformance of the Nasdaq is more of a sign that high-growth tech was ‘ahead’ of the curve… in the worst way. That said, since that post in May indices have fallen 11% or less, which makes me think we’re probably not quite at the capitulation stage yet. Some might argue that we are still in the denial stage (especially with Apple’s stock flat since May) but I think economic data has removed any potential for denial. Inflation has not come off meaningfully, the Fed is looking to hike the market into oblivion, there is no discussion of talks between Russia and Ukraine, and Xi continues his sabre rattling on Taiwan. The future does not look good. Thus, I do think if we weren’t there before we are probably somewhere in the panic/capitulation stage with regards to indices as a whole.

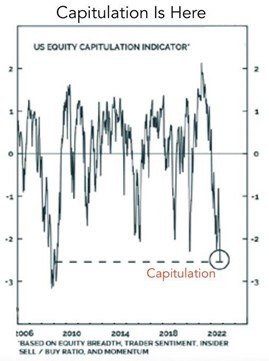

Now the question becomes: which stage is it? Is it panic or is capitulation? I don’t think there is a way to really tell with certainty, but there are some interesting charts worth going over. First, I saw this chart going around Twitter (link) a few days ago. It seems to imply that sentiment is at near-bottom levels, which I can certainly understand given my conversations with other fund managers lately.

This is also reflected by Bank of America’s Global Fund Manager Survey showing the highest cash levels (as a % of AUM) since the dot-com crash.

However, there are counterpoints that make me wonder if the capitulation is real. For example, Bank of America itself stated that just two weeks ago, client equity inflows were the third largest inflow since 2008. This implies that sentiment doesn’t mean much if positioning doesn’t reflect investor feelings. It could also mean that fund managers are being opportunistic and trading in and out of markets more frequently (but overall, cash levels remain are high). Another explanation at the so-called ‘smart’ money has sold already and that retail is still to do so (BoA has also stated that private client equity allocations are at ~60% of AUMs vs 40% in 2008).

An additional part of true market capitulation is the decline of all asset classes. We are starting to see this now with homebuyer demand crashing in the US (source) and energy prices in Europe coming back to 2021 levels (source).

We have also seen freight rates collapse as shipping bottlenecks clear, commodity prices generally decline, and bonds get decimated.

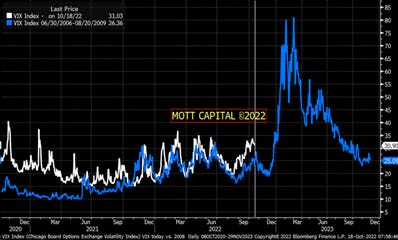

But to counter all of this, the VIX remains unusually low considering the consistent decline of the S&P 500 throughout the year (see chart below of the VIX compared to 2008).

We also have not seen any major bankruptcy in the corporate world, and GameStop is still trading significantly above its 2020 levels! Thus, I struggle to believe we are in a true capitulation stage for the market. I think we could still be in ‘panic’ mode, but as stated, certain pockets have moved far past that.

So now, we have to consider what investors should do if we still have at least a stage to go before the market starts a bottom. It’s a tough question to answer but clicking the “sell all” button is probably one of the wrong suggestions. Not all stocks will capitulate, and some already have (and so risk/reward has moved in their favor). Also, I could just be wrong and we might already be in the capitulation stage. So, here’s how I am thinking about the next few months with regards to the portfolio.

Don’t be dogmatic – if a business you own is not performing financially there is no need to add to it just because it’s cheap (cheap can always get cheaper). Trim it, sell it, reallocate. You don’t need to make back money the same way you lost if. If you strongly believe the long-term thesis is intact, you can hold, but prepare for pain (and some serious opportunity cost).

Cast a wide net – there are amazing opportunities in the market right now, but sticking to just what made you money in the past, is, I think, a mistake. Even after the market capitulates there’s no telling how long the basing part will take. So you probably have time, use it wisely to do solid research.

Increase your return threshold – you can get a near 4% return on your money risk-free, thus any investment you make here needs to be able to provide a significantly higher return for it to be worth your time. Thus slow-growing large caps are probably not the best place to fish.

Hedging and cash management are useful tools - use with caution, but do use.

Be nimble - I always smirk when I speak to someone who is sure about what the Fed is going to do (hike or pivot). Just a short-time ago the Fed wasn’t even “thinking about thinking about raising rates” and now everyone they are doing quite the opposite. I wouldn’t put too much faith in your Fed expectations, I don’t even think they know what they are doing. The point is the market is a bit like a 5-year old child right now, its highly suggestible. So any good (or bad) news, can send it sharply in any direction.

Keep perspective – while there could be more pain ahead, we are closer to the bottom now than any other time this year. The time to panic was probably 9-12 months ago. I think it's important for investors to keep calm. No good comes from staring at stock tickers all day.

On a happier note. This long- weekend we celebrate Diwali (Deepavali) in Singapore. It’s a time to see family, friends, relax, eat a lot, and celebrate the start of the new year. Take this time to maybe turn off CNBC/Bloomberg. So, to those of you who are celebrating – a very Happy Diwali to you and yours. And for everyone, celebrating or not, my wish is that this new year is better than the last!

Thanks for reading and happy investing.

Farrer Fun Fact

UnReal Estate: Take the data with a pinch of salt, but even if directionally correct, US Commercial Real Estate is in a world of pain (source, source).

Articles and Videos of the Week

Are Developed Markets now Emerging Markets? Maybe, just maybe. This thought provoking post explains further.

This new substack has excellent posts on some eclectic stocks. Its worth your time to check it out. (Not investment advice).

One of the reasons why I don’t believe that we are quite in the capitulation stage is because stocks like GoTo (Gojek) still trade at nearly 20x sales. To be fair this seems like a concerted effort by several parties to keep the stock pumped.

The Nasdaq Bank Index has been flat for nearly 20 years. See this. Investing is hard.

One for fellow Singaporeans, this great chart that explains how HDB value declines over time (scroll down a little).