Third World Efficiency

Third World Efficiency

This week we discuss efficiency in developing markets, visualize music royalties, and learn when to quit.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

I was in Mumbai last month, and on the final day of my trip I decided to get an MRI on my knee that I had been putting off for a while. My insurance in Singapore only covers in-patient treatment and I didn’t have the patience for going through the government system for what was a minor issue. So, on the morning of my final day, I decided to see if I could get the scan done on short notice. Within half an hour, I was on a video call with a doctor to whom I described my symptoms and told of my need for the scan. Within minutes of the call, the doctor had sent me a ‘prescription’ for the MRI over WhatsApp. I then called a nearby MRI Scan center which booked me an appointment for that afternoon. At my allotted time, I went to the center, and after an hour I was done with the scan in my hands. An hour after that, I received the clinical report by email. All of this was done at 10% of the cost I would have incurred in Singapore, and at lighting speed. Oh, my knee is fine, it turns out I’m just aging.

Developing markets can be a tricky place to live, work, and invest. Infrastructure needs significant work, traffic will make you tear your hair out, and corporate governance is only now becoming a concept discussed in board rooms. Despite all this, I’ve always been amazed by the ingenuity and efficiency of local economies and entrepreneurs to ‘leap-frog’ these issues and create extreme value for customers and consumers. My favorite example here is how accessible high-speed internet was in India when I worked there in my early 20s. You would think at the time, the country’s infrastructure could not handle fiber, and you would be right. It didn’t need to. Local internet providers just supplied customers with a dongle and thus ‘leapfrogged’ the need for the physical infrastructure to be in place. I used a dongle during my entire 2.5-year stint, and never felt ‘disconnected.’

There were a few other developments that surprised me during this visit to India, including the efficiency of delivery (due to abundant manpower) and the speed at which we got through immigration/customs/airline procedures driven by the privatization of the major airports in the country. Compared to the hours I’ve wasted at LAX or Heathrow, this was a pleasant surprise. However, this phenomenon of local efficiencies is not just an India story.

As a freshly minted college grad in 2008, I visited Brazil for about three-weeks. While cards certainly existed, cash was king. It makes sense, for a retailer cash is immediately available and has no transaction costs. However, it was not great for the consumer, for one it makes purchase of large order values difficult, and Brazil is not known for its safety (in fact, I was robbed at gunpoint on that trip). However, since then, Brazil has decimated cash’s market share of payments. In 2020, the central bank launched Pix, a payment method that allows for near instant transactions at zero cost to the consumer (minimal cost to the merchant). In just a few years since launch, Pix has become the most popular method of payment in Brazil – coming in at 30%, much higher than credit cards (20%) and debit cards (19%)[1]. The chart below from an IMF working paper shows how quickly the dominance of cash has dropped off in the country[2]. Granted, this is a public solution, but the bigger point is that there are several examples of deep efficiencies in developing markets.

While I’ve visited several countries on the African continent, I’ve never really considered it as a destination for investment. I will admit I’ve fallen prey to lazy group thinking here and adopted many of the stereotypes about the region. However, this write-up about Airtel Africa (not investment advice) had some fascinating stories about local efficiencies. While the thesis itself is interesting, I found the story of the adoption of mobile minutes as currency amazing. I paraphrase from the writeup;

“In sub-Saharan Africa, roughly 50% of the population still does not have a bank account… Individuals in Kenya started to solve this problem in the early 2000s by swapping cell phone airtime as a proxy for money. Researchers noticed this, and a solution was proposed whereby SIM holders could officially transfer money to each other. The pilot for M-PESA was rolled out by Safaricom (owned 40% by Vodafone) in 2005, and quickly became the dominant form of money transfer in Kenya.”

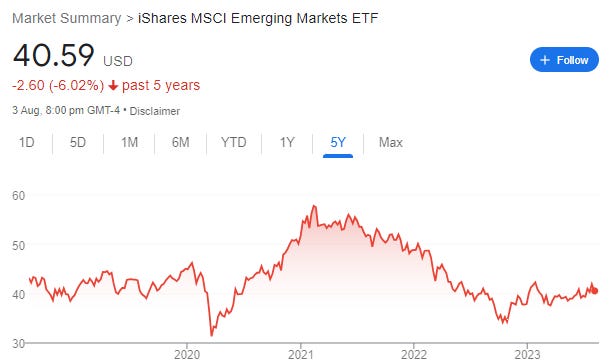

The bull case for investing in Developing/Emerging markets does not write itself. The 5-year stock performance of the MSCI Emerging Market ETF is a clear reason why. In fact, the ETF has been flat since around 2007.

But, anyone who has spent a moment investing in developing markets knows that it is a bottom-up game. There are plenty of examples of big winners in each of the sectors/countries mentioned above. To take a few; In Indian Healthcare, Max Healthcare has been a 5 bagger over the past 5 years (38% CAGR). In Brazil financials, the country’s oldest bank, Banco do Brazil’s stock has put up a ~19%+ CAGR total return over the past 20 years. While Airtel Africa has only compounded at 11% over the past 5 years, its EPS has grown 80% over the past 3 years and is expected to triple over the next 5 years.

Now the rub here is that most of the returns above are in local currency and that must be factored in. For example, any investment in India must almost assume a ~5% annual INR depreciation against the USD. While the Brazilian Real has been very stable against the dollar over the past 3 years, it lost half its value over the preceding 15 years. That said, even with that FX move, the Banco Do Brazil return is impressive (near 17% annualized in USD terms).

The point here is that many developing markets are really coming into their own with several well-run investable businesses. You need to separate the wheat from the chaff (i.e., perhaps Russia is off the table for a while) country-wise and be careful sector- wise (for every Max Healthcare there is a Fortis Healthcare) but opportunities are abound. Innovation is happening, efficiencies have been found, and developing markets are ripe for picking.

Thanks for reading and happy investing.

[1] https://www.fintechnexus.com/in-two-years-pix-became-the-most-used-means-of-payment-in-brazil/

[2] https://www.imf.org/-/media/Files/Publications/WP/2022/English/wpiea2022027-print-pdf.ashx

Farrer Fun Fact

Who owns what: I loved this visual representation of how the monetary value derived from a song is distributed across the creative chain. So next time you stream a song - you know where the money goes. (Royalty Exchange, source)

Links of the Week

I recently finished reading “Quit” by Annie Duke, which is an incredible book about when to “throw in the towel”. For those who don’t have time to read the book I highly recommend this essay by her instead.

This table is an excellent overview of on the difference between two payment giants, Stripe and Adyen.

Our friend/investor Rob Vinal recently visited China and wrote a ‘postcard’ containing his thoughts on the country that many foreign investors have given up on. Listen here.

Its long - over 3 hours, but this Acquired episode on Porsche was essentially a long-form investment writeup appendaged by its fascinating history. I thoroughly enjoyed it.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’. Thank you!

Attached you can find „the like“.