Winner of the Year

Winner of the Year

This year we discuss the best performing stock in our portfolio, take a look at a brutal year for the S&P 500, and give out a few h/t.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Latest Blog Post

Winner of the Year

We had to remove the ‘research’ section from our website for compliance reasons, but I miss disseminating our thoughts on individual securities and getting feedback on it. So as a year-end gift to ourselves (and perhaps our readers) we are going to discuss the best performing stock in our portfolio this year.

Please do remember this is not investment advice, we will not be giving any price targets, and please do not take any action on the below security solely based on this writeup. When it comes to valuation, we will also only discuss trailing numbers and street estimates. Further most figures are in local currency – so divide by 5 if you want a rough USD equivalent. Ok on to the writeup -

This ‘winner’, which is up 64% YTD in USD terms (as of 22nd Dec), is based in Brazil – yes you read that right. Despite a tough macroeconomic overhang, LATAM does produce several great companies – many of which investors in Southeast Asia have not heard of. Assaí Atacadista (“Assai”), which is the trading name for Sendas Distribuidora SA, is Brazil’s largest standalone cash and carry chain. For those unfamiliar with a ‘Cash and Carry’ (“C&C”) it’s essentially a very large supermarket that sells items in bulk. Think Costco, but without the membership requirements.

The Cash and Carry market in Brazil:

Besides their size, there are a couple key differences between a C&C business versus other retail formats such as hypermarkets, supermarkets, and convenience stores. For one, C&C businesses vary their inventory based on best pricing and availability. For example, you might come in to buy a large supply of beer, but what type of beer exactly could change from week to week. Second, C&C has a significant B2B component to it, where restaurants, smaller stores, school cafeterias will buy from the C&C business. This is particularly important in Brazil where bulk distribution is difficult, and most manufacturers rely on C&C business to reach business customers. Third, pricing is much cheaper and at times 13-15% less than other formats due to the ‘bulk’ nature of purchasing and selling.

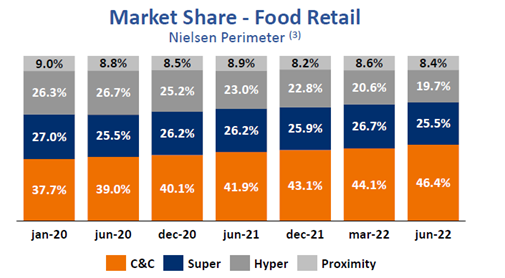

With regards to the industry in general, the C&C format has become more popular over the last few years as customers looked for both selection and value especially during difficult times during covid. C&C has about a 66% penetration in Brazilian households rising from about 59% in 2017 and is significantly more popular than other channels such as supermarkets (61%), hypermarkets (43%) and proximity stores (24%). Market-share of overall food spend has also increased and sustained post covid.

This store format is also especially suited for customers in Brazil, where the typical buying pattern of an average middle-class family comprises of large volume buying at C&Cs once a month. This is sometimes referred to as “Compra do mes” or purchase of the month. This habit is especially heightened in times of economic uncertainty when people need to control their budgets tightly. A majority of Assai’s clients for example come from Class C, D, and E social classes who have less than a R$3,152 (US$593) monthly household income.

There are several regional players in Brazil who operate C&C stores, however the two largest are Assaí with 233 stores and Atacadão which has 268 stores (Atacadão is larger but sits within the Carrefour Brazil group, Assai is the largest standalone player).

Assai’s History:

Assai was founded in 1974 as a wholesaler supplying to small businesses. The company was partially acquired (60%) by CBD (Cia Brasileira de Distribuicao, controlled by the French Casino Group) in 2007, before becoming a wholly owned subsidiary in 2011.

Since 2011, Assai began to invest in a new C&C (Cash & Carry) store format comprising large assortments of goods ranging over thousands of SKUs, self-checkout services and improved ambiance including covered parking, in-store WIFI, air-conditioning and natural lighting. From 2017, CBD’s C&C stores were formally transferred to Assai and were concentrated within the company.

Today, Assai is the 2nd largest retailer in Brazil, wholesaling food and non-food products to resellers, intermediate customers and individual customers, with a footprint in all but three states in Brazil. Retail operations are supported by 10 distribution centres in the Southeast, Northeast and Midwest regions of Brazil. The company serves over 30MM unique customers with more than 8,000 SKUs. About 100 stores also include high-value services such as butcheries.

Assai was spun off from CBD in March 2021 and listed on both the B3 (Brazil) and NYSE (as an ADR). The company was capitalized with R$7.8bln of debt and R$3.5bln of cash. Pre-spin, Assai contributed a sizable portion of CBD’s earnings, amounting to 40% & 70% of CBD’s sales & EBIT.

Assai is currently headed by Belmiro Gomes, who spent over two decades at Atacadão before coming over to CBD (as head of the C&C Business). Belmiro has an active presence online, frequently interacting with staff and new joiners on LinkedIn. He is also known to have a deep understanding of on-the-ground operations, and even noticing when checkout clerks are falling behind on throughput.

Inside an Assai Store:

Assai’s product offerings include common and basic brands, with a wide breadth of both fresh and packaged products. The company does not offer a wide variety of brands in any given category to ensure best prices for brands that are offered. Within Assai’s two pricing systems (“Atacado” and “Varejo”; “Wholesale” and “Retail”), the wholesale prices offered are ~12-13% cheaper than at supermarkets, encouraging customers to purchase more of each product to enjoy the cheaper prices.

The high ceilings and wide store aisles invoke a bulk-purchase shopping mentality for patrons, which encourages customers to buy more of each product. From an efficiency perspective, Assai’s store layout allows for increased storage capacity for the company, reducing the chances of any products becoming out of stock. With few shop assistants available through the store, Assai focuses sharply on customer self-service, providing with self-checkout counters to reduce labour costs.

Cumulatively, these initiatives are likely driving the company’s sales efficiency metrics. While there was a bit of a covid boost, this has also been maintained in a more normal world. As can be seen by this chart above, stores are becoming more efficient overtime, this despite the fact that Assai is in an expansion mode (more on that below) and most stores are still to mature.

Assai has a wide range of stores sizes ranging from 1,000 to 8,000 square meters per store. Stores typically take about 4-5 years to breakeven with full pay back around 6-7 years, Stores do about R$280mm/year at maturity with around a 6% (inc. leases) EBITDA. Capex per store is around R$65MM implying a 25% return on capital after maturity.

Financials:

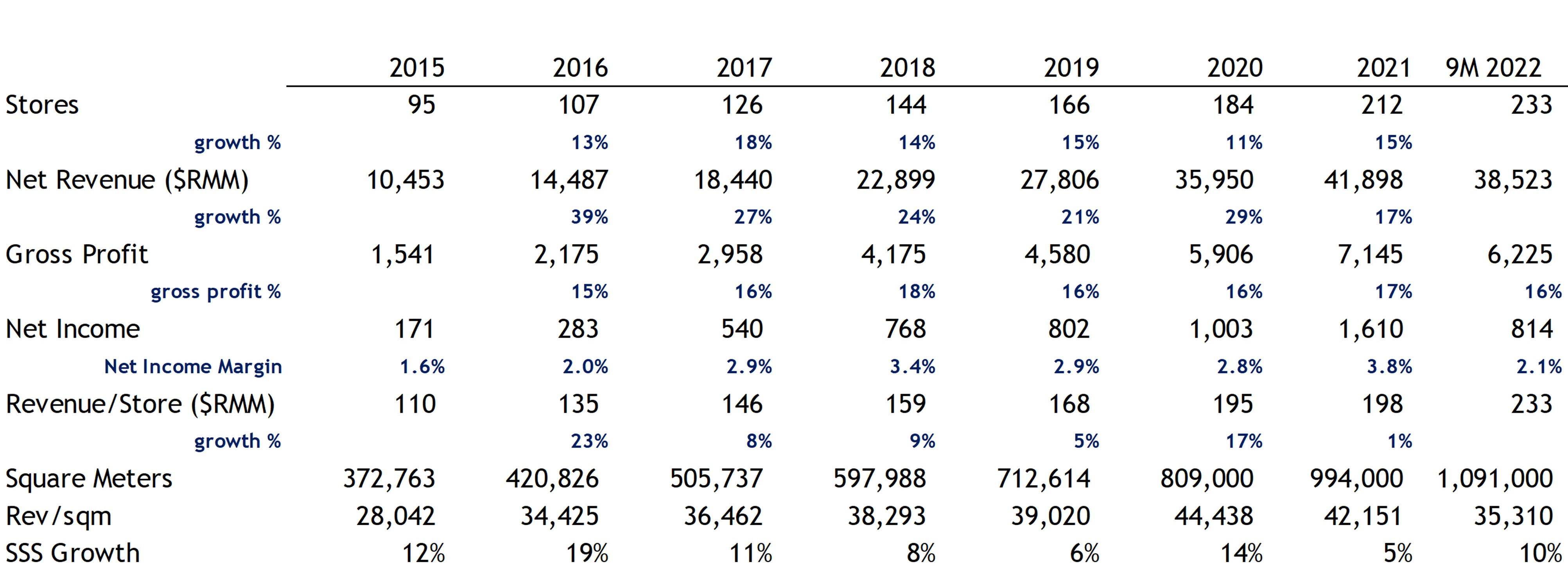

Assai standalone figures

As you can see from the above Assai has seen rapid net revenue growth of 25% compounded from 2015-2021 (inclusive) with same-store-sales growth continuing on an upward trajectory. Astute readers will notice Net Income coming off despite gross margins staying stable. This is because Assai has taken on quite a bit of debt to fund the acquisition it did of Extra Hiper stores (see below). As of Q3_2022 Assai has around R$7.8bn in debt versus R$2.8bn in trailing EBITDA (inc. lease expenses), so a ratio of around 2.8x. Further the Brazilian Central Bank has been ahead of the curve and raised rates aggressively in 2022, with current rates at 13.75%. The full extent of the rate hikes are yet to be felt in the Assai numbers as the interest rate they pay on their debt is based on an average trailing twelve month period. That said, we feel that Assai’s leverage will come off rapidly in the next few years as the conversion of the Extra Hiper stores completes (will be done by end 2024).

Extra Store acquisition:

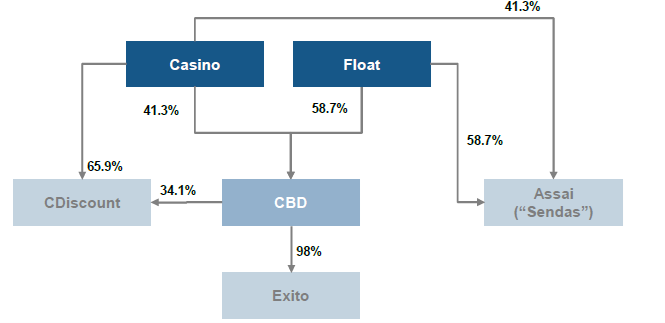

In October 2021 Assai announced it was acquiring 71 Extra Hiper Stores. These hypermarkets, owned by CBD were purchased for about R$4 billion. The pitch here is that these stores would add a total of R$25bn in revenue (thus a much higher rev/store of about R$350MM) and reach maturity much faster (~2 years vs 4-5 years). This is because these stores were already located in prime locations, had much of the infrastructure and inventory built out, and a customer base that already frequented the location. Margins are also slightly higher for these stores due to a smaller B2B component. Initially, this deal was met with a lot of skepticism as CBD (who Assai was spun off from) is also owned by the Casino group (Assai’s largest shareholder) (see image below).

The Casino Group (see risks below) does not have the best reputation and thus the market was naturally wary of the deal. However, the acquisition has worked out well with the conversion of the Extra Hiper stores moving ahead of schedule. This bolster on acquisition has also given management confidence that they will reach R$100bn in revenues by 2024 and with higher than current margins.

The Thesis:

So far, we’ve discussed that C&C is growing market share in Brazil, Assai is the second largest player (largest standalone) and is continually growing market share in its segment. The company is seeing increased efficiency on a store level, rapid growth, and steady-to-improving margins. Despite skepticism from the market, the Extra Hiper store conversion is going well. Brazil seems to be towards the end of its tightening cycle and any rate cuts would help both the debt burden and valuation. So, the ‘story’ itself looks quite compelling. Now let’s look at trailing valuations.

*EBITDA is pre-IFRS

As you can see above, Assai trades quite in line with its competitors (both Carrefour Brazil and Grupo Mateus have C&C businesses), despite much faster future growth. Grupo Mateus has a cheaper P/E multiple due to a lower debt load, but this will normalize as Assai’s debt comes off and/or rates get cut.

On an absolute basis the trailing P/E ratio for Assai looks high, but one must remember that they are in an expansion mode, and earnings are a bit depressed at this point due to the debt/interest. However, expectations (from the street) are that by 2025 Assai will do nearly R$3.5bn in earnings which would imply a 7.7x PE. The counter to that is that with interest rates so high, Brazil does face recession risk (especially with their GDP barely growing in 2022). However, given Assai is in the consumer non-discretionary space, it should hold up if there is a recession.

Looking forward, the market is starting to believe in Assai’s management targets of hitting Gross Revenue of BR$100bn (~$91bn Net Revenue) and 300 stores by the end of 2024. The street expects 7.6% EBITDA margins (post-IFRS) and 2.4% Net Income margin. 2025 expectations are about $104bn in net revenue with 3.3% net margins. Depending on what exit PE multiple you use (street is expecting anywhere from 13-17x), there is a chunk of upside left despite the large gains this year, however the margin is certainly lower than when we started to invest in the business.

Risks:

There are a few major risks to this business – some macro/Brazil related and some unique to Assai.

1) Casino Group ownership – this is probably the biggest pushback we get from other investors. The Casino group is a French mass-market retail conglomerate which owns cash & carry, hypermarkets, supermarkets, convenience stores etc. globally. The problem is the Casino Group does not have the best reputation for cash management and has had problems with debt for several years. It has had to seek bankruptcy protection in the past and the fear was that Casino would sell Assai shares to shore up their balance sheet. This, in fact, came true about a month ago, with the Casino group selling about 14% of outstanding shares and significantly reducing their previous 41% stake. Funnily enough the market took this as a positive as it also came with a shuffle to the board with one of Casino’s appointees stepping down, and Belmiro Gomes (the current and popular CEO) being added. There continues to be a risk that the Casino group might sell more of their shares, but it seems that the less influence Casino Group has the more the market likes the Assai stock.

2) Debt/Interest Rates – As mentioned Assai does have a reasonable amount of debt (around BR$ 7.8bn), but we think this is the max of it. Net Debt/EBITDA is around 2.8x and we will likely see this to start coming down rapidly within a year or so as the Extra Hiper stores conversions are completed. That said Brazil has an incredibly high rate of interest and this is not fully baked into Assai’s numbers yet (as mentioned above). But we do think that Brazil is likely at the end of its rate hiking cycle with rates having been held steady during the past few central bank meetings. So, while we will see Assai’s interest payments increase, we think this is likely to peak sometime next year and then come off if the central banks cuts rates. Inflation has come off rapidly though, coming in at 5.9% in November down from its peak of 12%. Even if rates are not cut, we expect free-cash flow to start flowing into the business by 2024. In fact, even after interest right now the company is putting up around R$1.6bn in cash flows over the past twelve months (over an EV of R$31bn) resulting in a 5% unlevered FCF yield. However, capex remains high with the conversion of Extra Hiper stores, but that should complete by 2024.

3) Brazil/CCY Risk – Brazil can be a tough place to invest given currency weakness, high inflation, and geopolitics. The Bovespa Index has only gained about 35% over the past 5 years in local ccy terms. However, unlike many countries this year, Brazil’s rising interest rates quickly has been a boon for its currency which has appreciated against the dollar over the past year. That said, currency weakness could occur (esp. if the central bank starts cutting rates) so any investment needs to take this into account. Further, Brazil just completed its presidential election which saw the return of Lula as the country’s leader. Lula is known to be quite socialist in his policies which has been reflected in recent weakness in the stock market. However, the election in general was not a clean sweep with many Bolsonaro loyalists getting elected to congress and as mayors of many cities. Thus, passing social legislation will not be that easy for Lula. That said, if he does manage to do this, and part of that includes giving more aid to the poor, this should only help Assai.

Conclusions:

We believe that Assai is a well-run company gaining market share in an imperative and recession proof (as much as one can be) sector. It has several years of growth ahead of it and while the ‘reward’ of the stock has been realized this year, we do think there is a good amount of upside left. The quality of the company seems to have been recognized with more onshore brokers covering it (it is part of the Bovespa Index after all), but we are yet to hear foreign investors spend much interest. A fun anecdote to reflect this was earlier in the year I was speaking to an investor based out of Brazil. I asked him how things were there given that we had an investment there. He asked if I had invested in Nubank (which is a popular Brazilian stock amongst foreign investors). I told him it was a company called Assai, to which he responded “Are you kidding me? I’m telling everyone I can to buy that stock.”

Thanks for reading, and happy investing. Wishing you and your family very happy holidays and the best for 2023. Until next year!

Farrer Fun Fact

A brutal year: S&P 500 2022 performance so far. A sea of red for the index’s worst year since 2008. (source)

Articles and Videos of the Week

As the year ends I wanted to highlight some of our friend’s work - excellent investors who post some fascinating ideas (posted below in no particular order). Add them to your list for 2023!

Asian Century Stocks - Excellent writeups on Asian stocks, and even if you don’t pay the very worth it ~$30/month - the free Monday morning links are always a goldmine.

Punch Card Investor - Detailed deep dives on companies like Sea, LVMH, Nvidia, etc.

Compounding Curiosity and Allocators Asia - Not just investing, but stories about businessmen, fascinating interviews, and much more with a focus on Asia.

310 Value - US/Europe focused value stocks

Yet Another Value Blog - I don’t actually know him, but tons of idea generation from the interviews he does with top investors.

And that’s a wrap! Thanks for reading and happy investing! See you in 2023.

Cheers Pratyush! Appreciate getting to finally catch up in person with you this year! Wishing you and ya family an awesome 2023.