Brain Damage

This week we talk stocks that do brain damage, analyze VC returns and listen to a deep-dive on AI infrastructure.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, data, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

Brain Damage

“This stock does brain damage” was what an investor friend texted me when we were both on an earnings call for a mutual holding. He was right - over the past year, the management of this company had changed directions twice, competition had heated up (illuminating the lack of moat around the industry) and the cap table changed quickly. The investment math quickly went from algebra to advanced calculus.

I’ve been thinking a lot about ‘brain damage’ stocks and how to spot them. You know it when you’re inveted in one – it’s the one that when a news alert comes out – your gut feel is that it’s likely to be negative rather than positive – it’s the one stock you track incessantly – it’s the one that gives you the most anxiety before earnings. It’s the one that when it comes out with bad news you may be surprised, but not shocked. It’s the one that when the price falls, the investorverse is filled with “told you so” or “it was so obvious.”

I’m sure reading this, one (or two) brain damage stocks in your portfolio come to mind. It's not a bad idea to hold such companies in your portfolio. Such stocks have the potential to provide for great long-term returns, but in the short-term they’ll make your hair turn grey.

Two examples may help contextualise the concept:

Kaspi: I spent some time earlier this year looking at Kaspi, which is a super-app in Kazakhstan. It has a 75-80% penetration rate in its country. It is a payments platform, a bank, a lender, offers travel and e-commerce services, and ubiquitous across the country (and some neighboring countries). Its revenue has grown ~50% on average over the last few years and the stock trades at just 11x P/E. But the company also has a murky relationship with the former President, ties to Russian money, and other red flags. For example, I felt that the sheer share of the country’s deposits/loans that were on Kaspi’s balance sheet was risky for a private player to hold. When going through my research I couldn’t help but think “this stock will do brain damage.” Just last week I was proved right – a short report was issued detailing Kaspi’s potential links to Russian money. Now, the short-report might be misguided but companies like Kaspi open themselves up to all sorts of commentary and the knee-jerk reactions that comes with negative news. I’m not saying this makes Kaspi a bad investment, and I wish shareholders the best. In fact, despite this report Kaspi is up ~100% over the past 4 years. It's just the path to the next double will likely be filled with more brain damaging news.

Haypp Group: Haypp is a Scandinavian online distributor of nicotine products (nicotine pouches and snus). It has an interesting moat around its business considering the likes of Amazon don’t sell nicotine products. Further, Haypp has real-time data which makes them the go-to-distributor for nicotine brands. The company has been growing like a weed (revenues also growing 50% on average over the past few years) has highly professional management (the CEO came over from British American Tobacco), and significant potential to grow past its core markets. I had a productive call with leadership, that made the investment even more intriguing. But the problem with the tobacco/nicotine industry is that it is in constant flux. Politicians want to either tax or legislate it out of existence. There is also data to show that even nicotine products aggravate cancer. A few weeks after the call with Haypp I woke up to an email from them saying that the city of Stockholm is proposing a ban on sales of traditional snus (pouched tobacco leaves). Snus sales in Sweden make up 20% of Haypp revenues. The stock subsequently fell 25%. Brain damage.

I want to be clear that I’m not picking on owners of the above company’s shares. I too have within my portfolio the cause of significant brain damage; a little company called Evolution. Evolution, for those unfamiliar, is the leader in live-casino games, and has some of the best margins of any company created. It has 70%+ EBITDA margins, near 55% net income margins, and has a 70%+ market share in its industry. However, because of the industry it is in and the markets it serves/conducts business from, this stock has negative news printed about it almost every six months. Whether it’s a short-report, regulators asking more questions, or worker strikes in its largest studio, you cannot own this stock and not have your heart skip a beat (and not in a good way) every half-year. The question is given all this – why own it? Well, the answer lies in my initial description of the company. It is simply a fantastic business, with strong/aligned leadership, trading at a cheap multiple considering its quality. The stock has 55x’d since its IPO in 2015, and the business continues to grow at double digits. Do I think Evolution will do well for the portfolio over the next few years? Yes. Will it also shave several months off my life? Also, yes.

Now a good question here is how you define a ‘brain damage’ stock. Its very easy to define any stock that experiences volatility as one that causes a near lobotomy. For example, Google is going through a phase of investors questioning its moat considering the rise of LLMs. But this is normal, every company has its moats/longevity/management decisions questioned. Eventually every company misses earnings. But I don’t think that does the damage we are talking about.

So, coming back to it, how do we define a ‘brain damage’ stock. Here I must rip off US Justice Potter Steward when he said he couldn’t define pornography but stated “I know it when I see it.” Similarly, it’s hard to define a brain damage stock. But here are some characteristics in a business to look out for.

Operates in an industry that is seen as damaging to society

Operates in (whole or part) jurisdictions where rule of law or where capitalistic/democratic values are not adhered to

Operates with too much leverage

Is going through a significant transformation

Management strategy shifts often

Management/Key Shareholder has a history of shady practices or associations

Management over promises and under delivers

CEO/Key Shareholder is highly public/vocal/opinionated especially about topics not concerning their business

Businesses also go from periods of causing brain-damage to tamer pastures. Meta did extreme brain damage in 2022 when Zuckerberg went full Ready Player One. Sea flip-flopped their strategy so much in 2023 that seasoned politicians were taking notes. But both those companies have done swimmingly since, and provided outsized returns. It is stories like these, and many like them, that attract investor attention and give credence to the below meme.

I’d be a huge hypocrite if I told you to stay away from brain damage stocks. They are exciting, can be hugely mispriced, and have the potential for outperforming returns. However, having too many of them in your portfolio will likely give you an aneurysm.

Thanks for reading and happy investing.

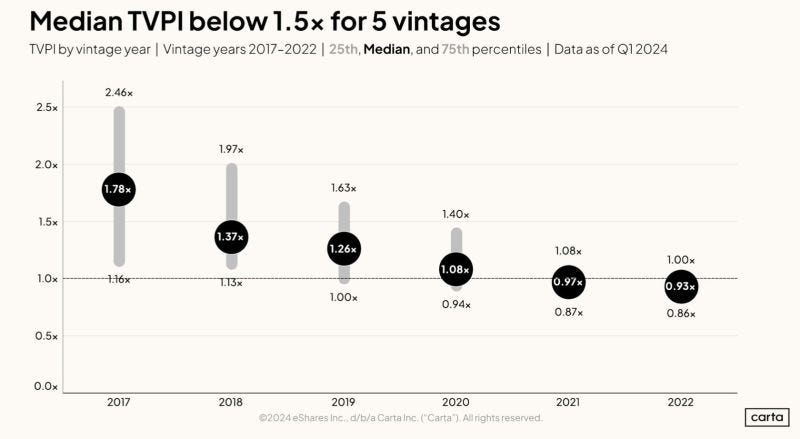

Chart of the Week

Venture Capital or Vanishing Capital? Data shows that newer VC vintages have struggled, and even the older ones are providing tepid returns on average (I believe returns presented above are before fees).

Links of the Week

Here is everything China did this week and what to expect going forward.

In this short clip, Apollo’s Marc Rowan discusses the move from public fixed income to private credit and why over the next few years he believes that there won’t be much of a difference.

Not sure how true this thread about Berkshire’s Todd Combs is, but even if its partially true its quite shocking.

Digital Bridge’s Marc Ganzi does a deep dive into the AI infrastructure opportunity in this 30 minute podcast.

Following up on last month’s post about Vietnam, the country has removed pre-funding requirements for foreign investors allowing for stronger flows into the country.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’ or share it. Thank you!

Don´t we all like a little brain damage

It is like the story in the last dance

https://www.youtube.com/watch?v=8m9XrJvJCBk

Interesting read

Thank you Pratyush for sharing