The Consolidation of Southeast Asia

The Consolidation of Southeast Asia

This week we comment on some fascinating events in SEA tech, speak 'honestly', and give tips on evaluating management.

Dear Clients and Friends of Farrer Wealth Advisors, we are pleased to bring you the Farrer Wealth newsletter, which includes our latest blog posts, fun facts, and general articles we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

The Consolidation of Southeast Asia

Disclosure: Farrer Wealth’s clients may have positions in the securities discussed below. The following writeup is for discussion purposes only, and is by no means, any sort of recommendation to buy, hold, or sell any of the stocks of the companies discussed below.

Picking up on last month’s piece on Sea, the last four weeks or so have brought up some interesting developments in Southeast Asia Tech worth writing about. These developments, concerning e-commerce and food delivery in the region, are potential positive harbingers, signaling the completion of a thesis for investing in SEA tech.

I’m getting a bit ahead of myself, so let me explain, going sector by sector.

E-commerce:

I attended Sea’s AGMs last week. It was a small (10 attendees) affair given that IR sneakily posted the announcement on their website just a few weeks before the event. However, for those in attendance it was a unique opportunity to ask questions directly to CEO, Forrest Li, who uncharacteristically answered almost all queries. There were a couple of noteworthy points relating to consolidation. For one, Li thought that the market in Southeast Asia is going to go through consolidation with only 2-3 players remaining. In his words, “it's hard being number four in this market.” We’ve already started to see this play out. Bukalapak, as we mentioned before, has been on the seller’s block for a while now. We’ve heard from many sources that GoTo needs more cash and is struggling to raise any more, meaning they will become a less important player in both ecommerce and ride hailing/food delivery (more on this later). The only two ‘stalwarts’, if you will, that have a high likelihood of survival is Shopee and Lazada (currently number one and two).

That brings us to the ‘threat’ of TikTok, which over the last four weeks has gotten a lot less ‘threatening.’ Most of you would be aware that Indonesia has rolled out regulation on social ecommerce that forces TikTok to separate its social and shopping functions into two different apps. Given this, TikTok has no choice but to turn toward just shelf commerce, and it might turn out that Indonesia is not worth it for them. They would have to spend even more on customer acquisition and will burn even more cash than they are now to regain any reasonable market share.

Even if this is not the case (let’s say TikTok decides to still play for the rest of SEA), Li mentioned something interesting in the AGM. He stated that while its early days, since they’ve started to re-invest in the market in July, they have both seen market share gains (which is to be expected) but more importantly, have not spent as much money as they thought they would have to. This is a sign that there is some modicum of maturity in the market, that despite competition, there is a moat and driven by a developed ecosystem and entrenched customers.

In my last month’s post about Sea, I postulated that perhaps ecommerce is just a terrible business and only makes sense in markets where there is consolidation (like in the Americas). But just four weeks later, we are at a crossroads. In scenario 1) TikTok decides without Indonesia, SEA is not worth it and exits the market. In this scenario it’s a three-way game between Shopee, Lazada, and Tokopedia (Goto). In this scenario I suspect Shopee runs away with it, despite Lazada’s more recent aggression. In scenario 2) TikTok decides to play for the rest of SEA (ex-Indonesia) and it’s a three-way game between Shopee, TikTok, and Lazada with I would think Shopee and TikTok in the #1 and #2 spots. I know as much as people want to believe TikTok is the Shopee killer, I think there are structural issues against this becoming a reality (I refer you back to my previous post). Given either scenario though, I think Forrest Li’s premonition is correct, this will end up being a 2-3 player market. While, there will always be barbarians at the gate (Coupang, Temu, etc) any consolidation will further entrench the surviving players, making the moat that much tougher for any invader to breach.

Food Delivery:

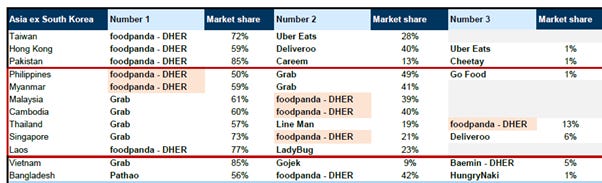

Another recent development was that Delivery Hero is mulling selling its APAC operations, which in SEA takes the form of foodpanda. Rumours are that Delivery Hero will sell foodpanda for ~$1bn, and Grab is one of the key suitors. Till date, the major regional players in food delivery have been Grab, foodpanda, Gojek (but this is mostly in Indonesia and Vietnam), and Line (Thailand). With the sale of the foodpanda business, especially to Grab, we will see significant consolidation in many markets. The chart below from Goldman shows how much market share Grab could own in the markets where Delivery Hero might sell foodpanda.

Essentially in the Philippines, Myanmar, Malaysia, Cambodia, Thailand, Singapore, and Laos (where Grab does not have operations), Grab could end up with 80-90%+ market share in food delivery. Considering the fact Grab already has a 70%-90% market share in ride-hailing, this will make them an even more formidable player in the SEA tech space.

Now Grab still must compete with Gojek in Indonesia, but if what we’re hearing is correct, Gojek will likely have to sell off its international operations (ride-hailing in Singapore and food delivery in Vietnam) which will further strengthen Grab’s position.

Grab is yet to break even, but it’s a given that this will happen soon. Even if they do buy foodpanda’s operations, I would think that this might delay profitability rather than stop it all together (While Delivery Hero’s Asia operations do post positive EBITDA, I suspect much of this comes from Korea). What I think this merger will do is potentially make Grab more profitable than the street expects, again driven by the consolidation in the space.

BNPL:

While I haven’t paid too close attention to this space off-late, I have observed a lack of crazy discounts/deals to use BNPL when I shop in Singapore. As far as I can tell most players have retreated to using BNPL behind their walled garden (ie using Shopee PayLater within the app), or are scaling down their operations. We’ve heard that Grab is mostly looking to take advantage of the cashflows in their system and only activating select customers. Shopback, which was noticeably the most aggressive, is putting weight on the BNPL break, and while I’m unsure of Atome’s strategy, it did exit Vietnam recently. It seems that rather than broad regional expansion, BNPL players are focused more locally, which again points towards consolidation within markets. While I don’t know the profitability levels of individual players, I do know that BNPL can be a highly profitable business if measured lending practices and reasonable marketing expenses are applied. Further consolidation should point toward a more profitable market going forward.

Again, I will caveat that I haven’t paid too close attention here, so if I’m wildly off, do correct me.

Consolidation – the end game?

Given the above, we’re starting to see (or will see) clear consolidation in ecommerce, ride hailing, food delivery, and perhaps BNPL. What will consolidation mean though? It means less expensive growth, more profits, higher penetration (companies can focus on new customers rather than solely on retaining older ones), new services, and ideally a better customer experience (surviving players can invest in logistics infra).

If this occurs – would this not be a complete win for investing in tech in Southeast Asia? We would have gone for unlimited funding and crazy spend, to rationalization of spend but lower growth, to steady growth and profitability via consolidation. Some might argue that many investors are still underwater in their Grab investments for example, but is that the fault of the company/market or the fault of overexuberant VCs?

If individual markets play out as above, this will validate the general tech thesis in Southeast Asia. Again, I know I’m being broad here and there is significant nuance, but isn’t this how successful startup investments are meant to play out? Certainly, there will be failures. I do think Bukalapak is a goner, and GoTo has serious issues, but failure is always going to be a case, and in my view, does not invalidate the thesis.

Now, regulation can be the fly in the soup. As much as Sea investors will be happy at the TikTok ban, the Indonesian government is likely not done. Given that, Sea (and Grab) is not Indonesian, any further protectionist policies will hurt. The LTA in Singapore is also reviewing ride-hailing regulations. Thus, this area (regulation) must be watched. But if all goes as predicted above, the next few years could be a renaissance for tech investing in Southeast Asia.

Thanks for reading and happy investing!

Farrer Fun Fact

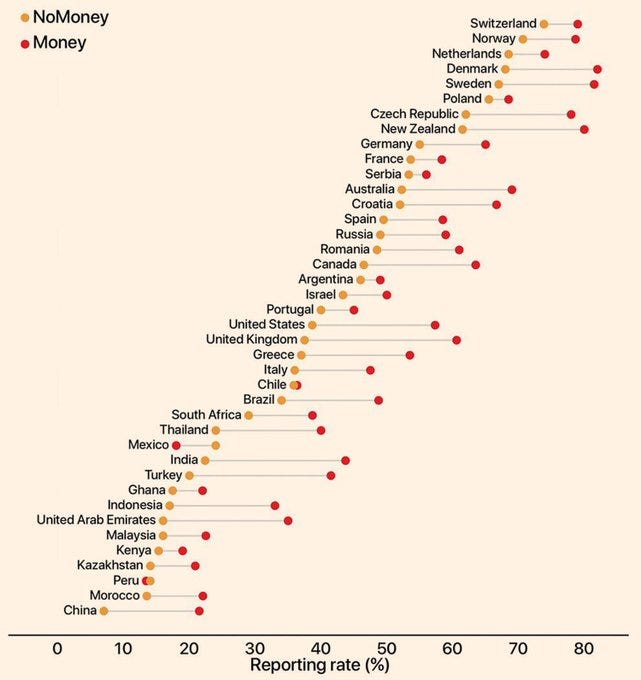

A measure of honesty? While there is a lot of nuance in the underlying study (so take this with a pinch of salt), this was a fascinating chart about the levels of ‘honesty’ in various countries. Researchers left 17,000 wallets (with contact email) containing various sums of money in 355 cities across 40 countries. The results, as expected, seem to be roughly correlated with how ‘rich’ a country is. But what was more fascinating, in almost every country there was quite a gap between wallets (with no money) returned, orange dot, to wallets (with money) returned, the red dot. Basically this implied the more money that was lost, the more likely return was. What’s also fascinating is the few countries where that trend was reversed (ie Mexico). Again, not entirely related to investing, but I would imagine there is some correlation here with corporate governance within countries. (source)

Links of the Week

Jon Kingston has been publishing this great piece every week or so that highlights dozen+ stock pitches from fund managers. Its a great way to find new ideas (not investment advice)

Morgan Housel was on the Odd Lots podcast speaking on how major events shape the way we think about money. Give it a listen this weekend.

This was an interesting thread on why and how to evaluate management of a company.

I’ve written several times about the issue of declining birth rates across the globe, this infographic points to how dire the issue really is.

GenZ is redefining work, and this video (10 mins), explains how.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’. Thank you!